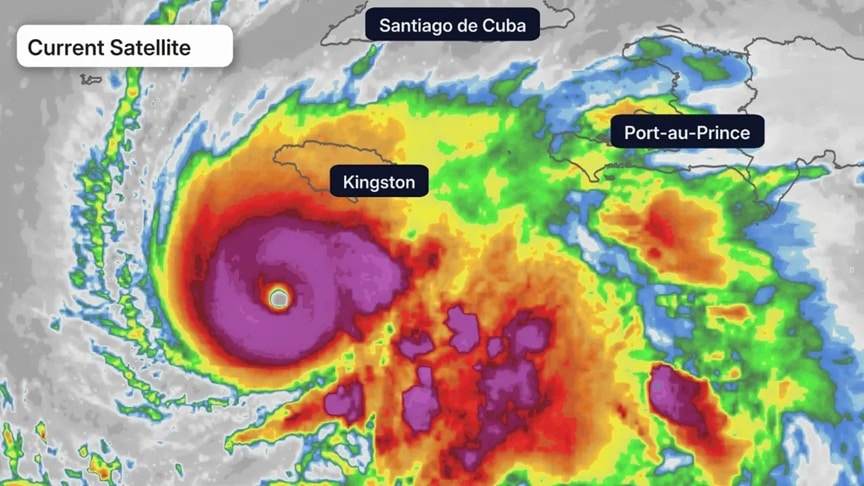

Hurricane Melissa has begun what meteorologists are calling a catastrophic, multi-day flood and wind siege across Jamaica. According to The Weather Channel, Melissa is expected to be one of the most intense, devastating hurricanes on record for the island, unleashing destructive winds, widespread flooding, and landslides. With Hispaniola and Cuba also in the storm’s path, forecasters warn of grave flooding concerns as the system slowly churns north.

While the headlines focus on Melissa’s Category 5 status, insurance professionals know that the real story begins once the winds die down — when the claims process starts. And here’s the twist: insurance payments are not triggered by the hurricane’s category level, but by the damage it leaves behind.

The Damage, Not the Category, Triggers the Claim

It’s a common misconception that a hurricane must reach a certain category — such as a Category 4 or 5 — for insurance or reinsurance payments to activate. In reality, insurers assess physical damage, not storm classification.

Even a Category 1 hurricane can trigger claims if it causes structural damage or loss covered under a policy. What matters is the event’s impact on property and infrastructure — not its wind speed rating on the Saffir-Simpson scale.

For reinsurers, the category may serve as a risk indicator, but claims are driven by reported losses, not by the numerical label attached to the storm.

Deductibles Are the Real Trigger Point

When a named storm like Melissa causes damage, hurricane deductibles come into play. These specialized deductibles apply specifically to windstorm losses caused by named hurricanes and are percentage-based, often ranging from 1% to 5% of the policy limit.

For example:

- In high-risk coastal regions, a homeowner with a $500,000 dwelling limit and a 5% hurricane deductible would face a $25,000 deductible before insurance kicks in.

- In inland areas, deductibles may be lower or expressed as a flat dollar amount.

The critical point: a Category 5 hurricane doesn’t automatically waive or reduce the deductible. Only if the total loss exceeds policy limits might the insurer effectively absorb the deductible as part of a full payout — but that’s an outcome of total destruction, not an exception to policy terms.

Why Category Still Matters — Just Not for the Reason You Think

Melissa’s record-breaking strength matters because it raises the likelihood of large-scale damage — not because it automatically triggers coverage.

Categories 3–5 hurricanes tend to cause widespread destruction, from roof loss and power grid collapse to business interruption and flood-related losses. But many smaller hurricanes, such as Category 1 or 2 storms that stall or dump massive rainfall, have historically produced catastrophic damage and equally large claims.

For insurers and reinsurers, Melissa’s classification signals the potential for heavy exposure, but the claims process will hinge entirely on verifiable losses.

Check Your Policy — Know Your Deductible

The details of hurricane coverage and deductible triggers are spelled out in your policy. Policyholders should:

- Review how their insurer defines a “hurricane deductible trigger” (some policies activate when a named storm makes landfall; others when watches or warnings are issued).

- Confirm whether the deductible applies per storm, per policy period, or per calendar year.

- Understand exclusions — for example, flooding from storm surge may require separate flood insurance through the NFIP or a private carrier.

Being proactive now prevents unpleasant surprises after the storm.

Final Takeaway for Agents and Insurers

As Hurricane Melissa continues its destructive march across Jamaica and threatens nearby nations, the insurance industry braces for what could be one of the costliest late-season hurricanes in recent memory.

But amid the chaos, it’s essential to communicate one message to clients and the public alike: Insurance payouts are determined by damage — not by the storm’s category.

Understanding hurricane deductibles, maintaining up-to-date coverage, and knowing policy limits are key steps in recovery readiness. For agents and brokers, Melissa is a real-time reminder to help clients translate media hype into actionable policy awareness.

Satellite image: The Weather Channel

Stay informed and ahead of the curve — explore more industry insights and program opportunities at ProgramBusiness.com.