Housing affordability in the United States is increasingly shaped by factors beyond home prices and mortgage rates. New data from the Cotality Housing Affordability Index shows that rising insurance premiums, escalating property taxes, and private mortgage insurance are now central drivers of affordability pressure nationwide.

In many markets, these costs make up more than 40% of a buyer’s total monthly housing obligation. As a result, affordability constraints have expanded well beyond traditionally high-cost coastal regions and now affect a broad range of Core-Based Statistical Areas nationwide.

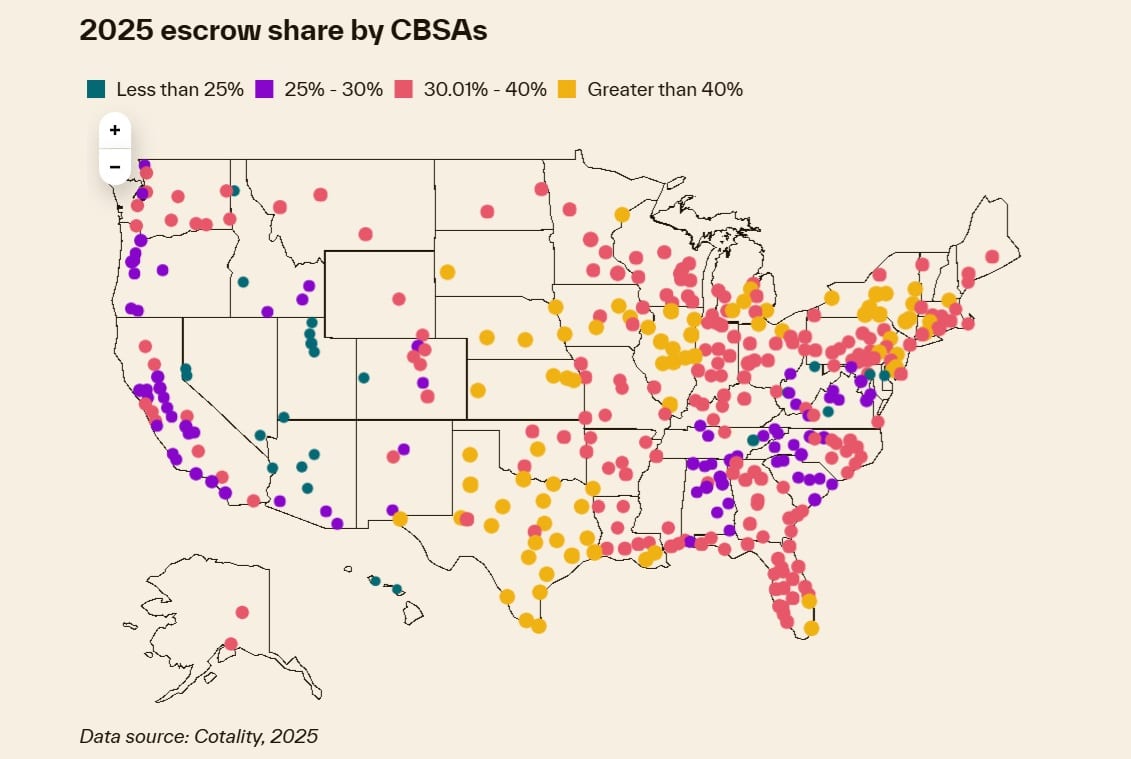

The Rise of the Escrow Burden

Cotality data points to a growing “escrow burden,” defined as the combined cost of property taxes, insurance premiums, and PMI. In several markets, this burden now outweighs the mortgage payment itself.

This trend is especially visible in the Midwest and Northeast. Texas illustrates the dynamic clearly. While many Texas markets appear accessible based on median sale prices, high property taxes and insurance premiums materially increase total ownership costs. According to Cotality experts, these costs function as a hidden tax that reshapes affordability once escrow expenses are factored into monthly payments.

The Cotality Housing Affordability Index incorporates these escrow costs directly into its calculations, highlighting how ownership affordability has shifted in recent years. What once appeared affordable on price alone often looks very different when taxes and insurance are factored in.

A Shrinking Pool of Affordable Markets

The expansion of escrow-driven costs has coincided with a sharp contraction in the number of affordable housing markets nationwide. Over the past decade, the number of affordable CBSAs declined by 40%, falling from 354 in 2014 to 212 in 2025.

At the same time, markets categorized as “high affordability,” defined by an index value of 200 or higher, have nearly disappeared. In 2014, 41 CBSAs met that threshold. By 2025, only four remained.

This shift has produced what Cotality describes as an “affordability desert.” Much of the West Coast and major Eastern hubs, including New York City and Miami, now sit firmly below affordability benchmarks. Median-income buyers increasingly find access only in parts of the Midwest and select areas of the South.

Under the CHAI framework, an index value above 100 indicates that a median-income family can afford a median-priced home. An index below 100 indicates that affordability has slipped out of reach for more families. The latest data show that fewer markets meet or exceed this baseline than at any point in the past decade.

Income Disparities Reach Historic Levels

The affordability gap between markets has also widened significantly. In Anaheim, California, a buyer needs an estimated annual income of approximately $319,000 to support a monthly housing expense of $7,974. In contrast, homeownership in Johnstown, Pennsylvania, remains accessible for households earning $32,000 or less.

This means a buyer in Anaheim requires nearly 10 times the income of a buyer in Johnstown to enter the market. According to Cotality, this disparity represents a historic high and underscores how unevenly housing costs now distribute across regions.

These differences reflect not only variations in home prices, but also sharp contrasts in insurance premiums and property tax structures. In higher-cost markets, escrow expenses compound already elevated prices, pushing required incomes well beyond local medians.

Local Affordability Versus Outside Capital

Cotality notes that affordability is inherently relative. A market that appears unaffordable to local residents may still present opportunities for buyers relocating from higher-cost areas.

Migration patterns continue to reflect this imbalance. Buyers from California, often leveraging accumulated equity, can outbid local buyers in markets such as Arizona and Nevada. This dynamic tightens conditions in destination markets and extends affordability challenges across state lines.

As these patterns persist, the impact of escrow costs becomes increasingly national rather than regional. Rising insurance premiums and property taxes follow buyers into markets that previously maintained lower ownership barriers.

How the Index Measures Affordability

The Cotality Housing Affordability Index measures an average family’s ability to purchase a median-priced home within a specific market and time period. The methodology builds on the National Association of Realtors affordability index, with adjustments based on Cotality analysis.

The index incorporates escrow costs directly into the monthly payment calculation. Escrow expenses include property taxes, insurance premiums, and private mortgage insurance when required. Cotality derives these figures from its Loan Level Market Analytics data.

The index expresses affordability as a ratio of median family income to qualifying income, multiplied by 100. A value of 100 indicates that a median-income household has just enough income to afford a median-priced home. Values above 100 indicate greater affordability, while values below 100 indicate reduced affordability.

Key assumptions include a 15% down payment based on median home prices from Cotality property record data and a 30-year fixed mortgage rate derived from Freddie Mac averages. The model assumes that total monthly housing costs, including principal, interest, taxes, and insurance, should not exceed 30% of household income. Median family income figures come from the FFIEC Median Family Income Report.

A Redefined Affordability Landscape

The latest CHAI data shows that housing affordability is no longer driven solely by mortgage rates or listing prices. Instead, the growing weight of taxes, insurance, and PMI now plays a defining role in who can enter the housing market and where.

As escrow costs continue to rise across a wide range of CBSAs, the geography of affordability is shifting. The result is a housing market increasingly defined by total ownership costs rather than just the purchase price.

Get the latest insurance market updates and discover exclusive program opportunities at ProgramBusiness.com.