A pair of small Pennsylvania insurers focused on long-term care could soon become one of the nation's costliest insurance failures ever, highlighting the widespread problems that have plagued the industry niche for more than a decade.

A pair of small Pennsylvania insurers focused on long-term care could soon become one of the nation's costliest insurance failures ever, highlighting the widespread problems that have plagued the industry niche for more than a decade.Two insurance units of Penn Treaty American Corp., which have combined assets of about $600 million and projected long-term-care claims liabilities topping $4 billion, are on track to be liquidated early next year, according to filings in a state court in Harrisburg.

While details are still being worked out, a liquidation is likely to be the second-largest life-health-insurance insolvency in U.S. history by assessments, according to officials with a network of industry-funded guarantee associations. An assessment is the amount other insurers are required under state laws to pay to cover policyholders of a defunct firm.

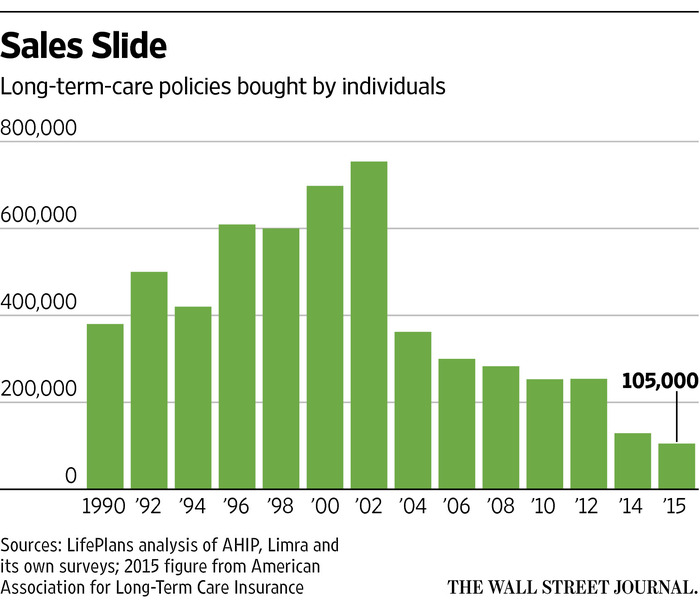

From the 1990s through the early part of the last decade, dozens of insurers sold long-term-care policies, viewing the then-new product as a growth engine that would address aging middle-class Americans' worries about paying for care later in life. The policies pay for personal aides and extended nursing-home stays that Medicare, the federal health-insurance program for the elderly and disabled, doesn't generally cover. The federal-state Medicaid program does pay for nursing homes, but is available only to the poor.

But most actuaries badly underestimated costs, and the insurers then met resistance in many state insurance departments when trying to push the pricing miscalculation onto policyholders through steep rate increases. Some states did allow double-digit-percentage increases, distressing the often-elderly policyholders. Sales have collapsed amid the turmoil, and fewer than a dozen insurers sell any significant volume today.

"Penn Treaty is the poster child for what happens if everything goes wrong-when key assumptions on...claims, morbidity and interest rates go wrong-and then companies are unable to get justified rate increases," said Gary Hughes, general counsel for the trade group American Council of Life Insurers.

The two Penn Treaty insurers have about 79,000 long-term-care policyholders. About 10% of them could lose some benefits in the long run, as most states cap the amount payable to individuals, possibly amounting to hundreds of thousands of dollars in some instances, guarantee officials said.

"The whole bottom fell out of my life," Michelle Leonard, 64 years old, a former college professor and administrator in Florida now out on disability, said of Penn Treaty's downward spiral. She anticipates filing a claim in the future and could receive the benefits she has counted on, but a lack of certainty is causing anxiety.

Pennsylvania regulators first sought to liquidate the two insurers in 2009 as their problems deepened, which they resisted in favor of rate increases. Penn Treaty "is pleased that years of litigation have successfully concluded," said Douglas Christian, a partner with Ballard Spahr LLP, who represents the company.

The long-term care policyholders in the two Penn Treaty units total roughly 1% of some 7.2 million across all insurers, according to the American Association for Long-Term Care Insurance, a trade group for agents.

But assessments on other insurers to help pay the Penn Treaty benefits are estimated at $2.58 billion, reflecting the state caps. That approaches the record $2.9 billion for Executive Life Insurance Co., according to the National Organization of Life & Health Insurance Guaranty Associations. Executive Life was a large California life insurer before its holdings of high-yield debt plunged in value in the early 1990s.

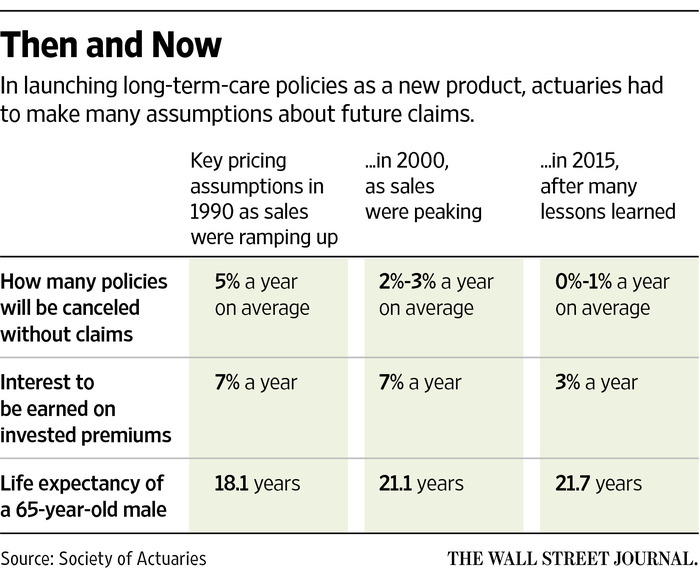

In launching long-term-care, insurers' actuaries had to make assumptions about matters such as the number of people who ultimately would file claims and how long they would need care before dying. Insurers also had to estimate how much interest they would earn on invested premiums, a figure that collapsed as the Federal Reserve has kept rates near zero since 2008.

In one of the biggest early mistakes, many insurers assumed some 5% of policies on average would lapse annually, meaning policyholders would drop them or die without filing a claim. Under this assumption, after 20 years fewer than 400 of every 1,000 policies originally issued would remain. Instead, just 1% or so of customers each year let their policies lapse, leaving 800 or more still in place.

"The big unknown was how the insured population would use long-term care," said Vincent Bodnar, chief actuary at LTCG, a third-party administrator of long-term-care policies. Among lessons learned: Owners view their policies as a valuable investment.

The Allentown, Pa.-based Penn Treaty insurers made a big push into the product in the 1990s, with rates lower than some competitors but approved by state regulators. They were smaller and less diversified than many rivals, so had less ability to absorb pricing miscalculations.

Pennsylvania regulators in January 2009 obtained a court order to "rehabilitate" the insurers into better financial condition. Nine months later, they sought permission for liquidation, arguing the balance-sheet hole was too big to plug with rate increases. But the court ruled in 2012 against the regulators.

The state lost its appeal. Meanwhile, the two insurers' finances worsened, leading to an agreement this year on liquidation.

The assessments will largely apply to health insurers because long-term care is considered a type of health insurance under most state laws. Harold Horwich, a lawyer representing Aetna Inc., Cigna Corp., UnitedHealth Group Inc. and other health insurers, said in a Nov. 9 court hearing that the health insurers were "in the process of finalizing negotiations over a very comprehensive settlement with the guarantee associations."

Guarantee associations in most states cap payments to long-term-care policyholders at $300,000, while two-Missouri and Oregon-limit it to $100,000.

"It's absolute disappointment that what we had planned" in the 1990s is working out so poorly, said Leaton Williams III, a 75-year-old retired federal employee. He and his wife bought Penn Treaty policies with inflation-adjusted, lifetime benefits, and now he fears they will exceed the $300,000 per-policyholder cap of the association in North Carolina, where they live. "It's really frustrating."